The last decade has largely belonged to US equities, particularly the technology giants that have come to dominate global markets. Buy a global equity fund and a large chunk of your money ends up in the United States, particularly the megacap technology companies.

But with increasing US political instability, relatively high valuations and the thread of a sliding dollar, investors are asking whether they should have more exposure to emerging markets.

After all, that’s where much of the world’s population lives, where economic growth is often strongest, and where many of tomorrow’s global champions may emerge.

This has played out in financial terms lately. In 2025, the MSCI emerging markets index grew 17.8%, whereas developed markets grew 6.8%. The trend has continued this year, with emerging markets up 14.7%, vs 5.8% in developed markets.

So what does “emerging markets: actually mean, and should you have a bigger piece of them in your pension and investments?

What are emerging markets?

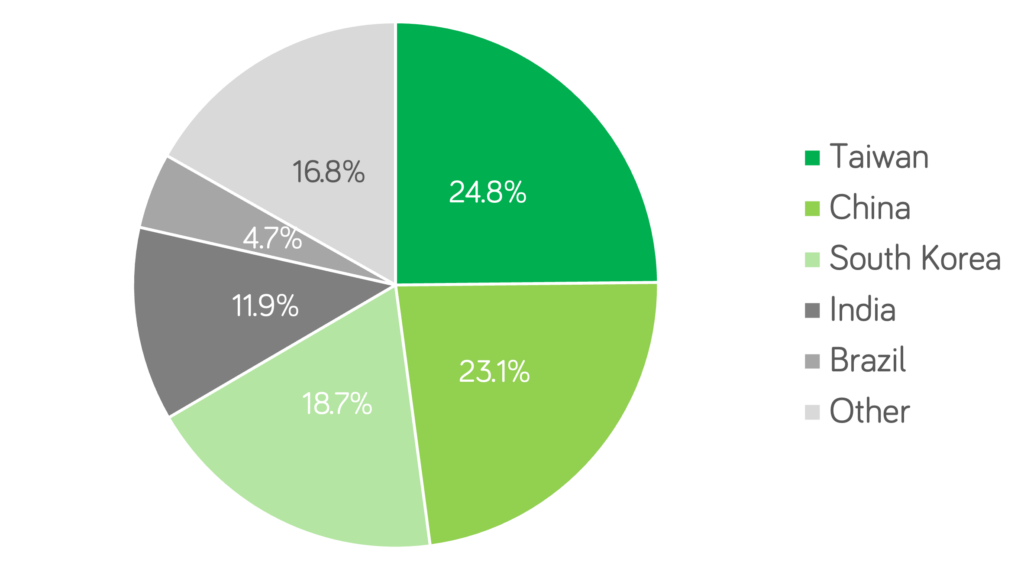

Most investors think of emerging markets (EM) as fast-growing economies such as China, India and Brazil.

That is broadly correct, as the chart shows.

The label hides a surprising amount of diversity.

The major emerging market indices also include countries such as South Korea and Taiwan, which are highly advanced economies with world-leading technology sectors. They include wealthy, oil-driven Gulf states such as Saudi Arabia and Qatar. And they include countries within the European Union, such as Greece and Hungary.

There’s a strong tech element, with Taiwan Semiconductor, Samsung and chipmaker SK Hynix making up nearly a quarter of the index. But financial services, consumer stocks, energy and industrial companies and healthcare services also feature.

It can seem like an odd collection.

Emerging market classifications were originally designed by index providers to reflect factors such as market accessibility, regulatory standards, liquidity and capital controls rather than simply economic development and the kinds of companies.

As a result, some countries that most people would consider developed remain classified as emerging markets, while others have moved between categories over time.

This makes “emerging markets” a less useful concept than it once was. Increasingly, investors are buying exposure to a collection of very different economies rather than a single coherent asset class.

Why are emerging markets attracting attention right now?

There are several reasons why investors are taking another look.

First, many emerging economies benefit from higher commodity prices. Countries such as Brazil, Saudi Arabia and South Africa are major exporters of energy, metals and raw materials. A stronger commodity cycle can provide a significant boost to growth and company profits.

Second, a weaker US dollar tends to support emerging markets. Many emerging economies borrow in dollars or rely on dollar-based trade. When the dollar weakens, financial conditions often become more favourable.

Third, investors are increasingly hopeful that China may be emerging from a prolonged period of economic weakness. Given China’s weighting at almost a quarter of emerging market indices, even a modest recovery would have a significant impact.

There are other factors too.

Valuations in many emerging markets remain lower than those in the US, offering scope for growth. Demographic trends are favourable in countries such as India and Indonesia, where younger populations are supporting economic growth, and a rising middle class can drive consumption. And governments around the world are diversifying supply chains away from a heavy dependence on China, creating opportunities for countries such as Vietnam, Mexico and India.

Is there more risk in emerging markets?

Usually, yes.

Emerging markets tend to be more volatile than developed markets. Political instability, weaker corporate governance, currency fluctuations and less mature financial systems can all create additional risks versus investing into mature markets like north America and Europe.

Investors also need to remember that economic growth does not always translate into stock market returns. Fast-growing economies can still produce disappointing investment outcomes, for example if company valuations are too high (for example in the case of China’s property crisis over the last five years) or if profits fail to reach shareholders (for example in the case of corruption scandals in South Africa).

That’s one reason emerging markets have often lagged expectations despite strong economic growth.

How much should you allocate to emerging markets?

Some commentators argue that emerging markets deserve a much larger allocation because they account for a significant share of global GDP and population.

But stock markets don’t reflect population; they reflect investable companies.

Today, emerging markets represent approximately 12% of the global stock market, with a combined market capitalisation of around $11.6 trillion out of roughly $99 trillion of listed companies worldwide.

For most investors, that is probably a sensible starting point.

Could you justify a modest overweight position? Potentially. But avoid thinking of emerging markets as a single investment theme. The category contains everything from Taiwanese semiconductor manufacturers to Saudi oil companies and Indian banks.

If you’re going overweight EM, an actively managed exposure to a subsection of EM could make sense – for example, a commodities exposure or a regional exposure to Asia-Pacific.