Knocking years off your mortgage is not always the most efficient use of your spare cash. We’ve been speaking to the Sunday Independent to explain why.

We ran the numbers on four options: keeping your cash in the bank, paying down the mortgage, investing the cash, and putting it in your pension.

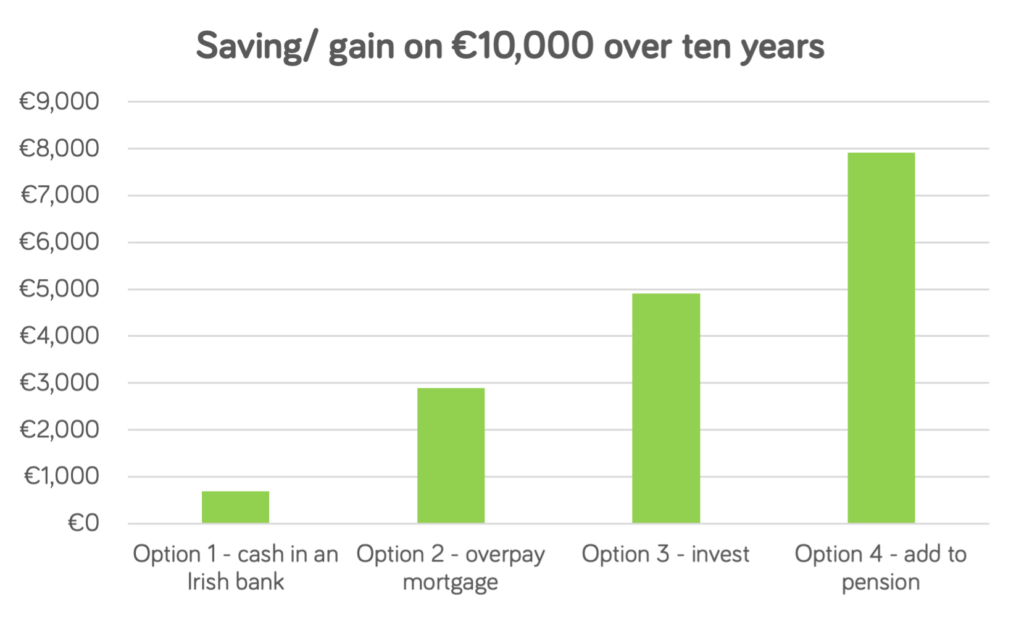

Your €10,000 will make most money in a pension, and least in the bank

Option 1 is simple. Cash in the bank will be there when you need it, and there’s little chance of investment losses. At the other end of the scale, there’s option 4. With a pension, there’s a tax tailwind, and you can assume that on average, decent investment growth can be had.

As the chart below shows, topping up your pension makes the most money for most people, while cash in the bank makes the least. That’s not surprising: the paltry returns on cash in the bank are well-known.

In contrast, pension investments can move up and down dramatically over the short term – and you’ve likely locked up the money until you’re 60.

But delve deeper and it’s clear the decision is not clear-cut.

Mortgage overpayments offer a guaranteed saving

If you were putting that lump sum of €10,000 towards a one-off overpayment on a mortgage of €250,000 with 20 years remaining and a rate of 3.5pc, you’d gain €2,888 after 10 years.

That dwarfs the €691 you’d have after a decade if you’d stuck the €10,000 into a notice deposit account at an Irish bank earning interest at 1pc.

Alternatively overpaying a mortgage offers a guaranteed and immediate saving on interest.

What’s more, it’s simple, and you don’t have to worry about taxes on savings, taxes on investments, or fret about volatility in the financial markets.

Could you access a lower interest rate by overpaying your mortgage?

Overpaying your mortgage offers some additional potential benefits too. Paying down a lump sum – perhaps together with a rise in the value of your property since you bought it – could mean that your loan-to-value ratio crosses a threshold to access a lower interest rate.

For example, say you bought a €500,000 property with an 80% mortgage some years ago. Perhaps now its value has risen to €600,000, while you’ve paid down 7.5% of your mortgage.

Paying a €10,000 sum now would mean your mortgage is now at 60% loan-to-value, a point at which lenders often offer better rates. You could lob in the lump sum and fix your mortgage rate on new terms. This could be attractive if interest rates rise during 2026, a situation which looks increasingly likely as inflation spikes in the wake of the Iran conflict.

Before you make a mortgage overpayment, make sure you talk to your lender to be sure there are no penalties for overpaying.

With mortgage overpayments, your money is tied up

Overpayments on your mortgage are illiquid: you can’t access those funds without selling the property or using its increased equity to take out a loan. Once you’ve paid money off your mortgage, you can’t get it take it out again – for example if you need cash for other purposes.

Investing: the middle ground

That leaves option 3: instead of spending that €10,000 on reducing your mortgage balance, that cash would be worth €17,908 in 10 years’ time if you’d invested it in a globally diversified fund, at conservative annualised growth rate of 6pc (after fees).

After paying tax and fees, your return would amount to €4,488 – substantially in excess of the mortgage interest saving of €2,288.

Our conclusion? Often the answer is a little bit of everything, as you build several pillars to your wealth. If you have, say, an extra €1,000 to spare, you could overpay your mortgage by €400, put €400 into a pension, and invest the remaining €200 into a liquid fund for medium-term growth.

This piece is adapted from an article which appeared in the Sunday Independent on 22 March 2026.

Key assumptions in calculations

Amount of spare cash to invest/ overpay: €10,000

Bank interest rate: 1%

Annualised investment growth on investment/ pensions after fees: 6%Tax rates remain constant

Dirt 33%

Exit tax 38%

Tax relief on pension 40%

Interest rate on loan 3.50%

Years left on loan 20

Amount outstanding 250,000

Overpayment 10,000