At the start of the year, we suggested that AI excitement would spread to new markets, that interest rates could rise, and that alternative assets would offer portfolio resilience in a volatile environment. Well, that all proved correct – and it only took six months. On top of that we had war in the Middle East, a new energy shock, and the biggest stock market flotation in history.

Where to from here? Read Moneycube’s midyear market review 2026 to get our take on the year so far, the outlook from here, and understand where we see risk and opportunity in the months to come.

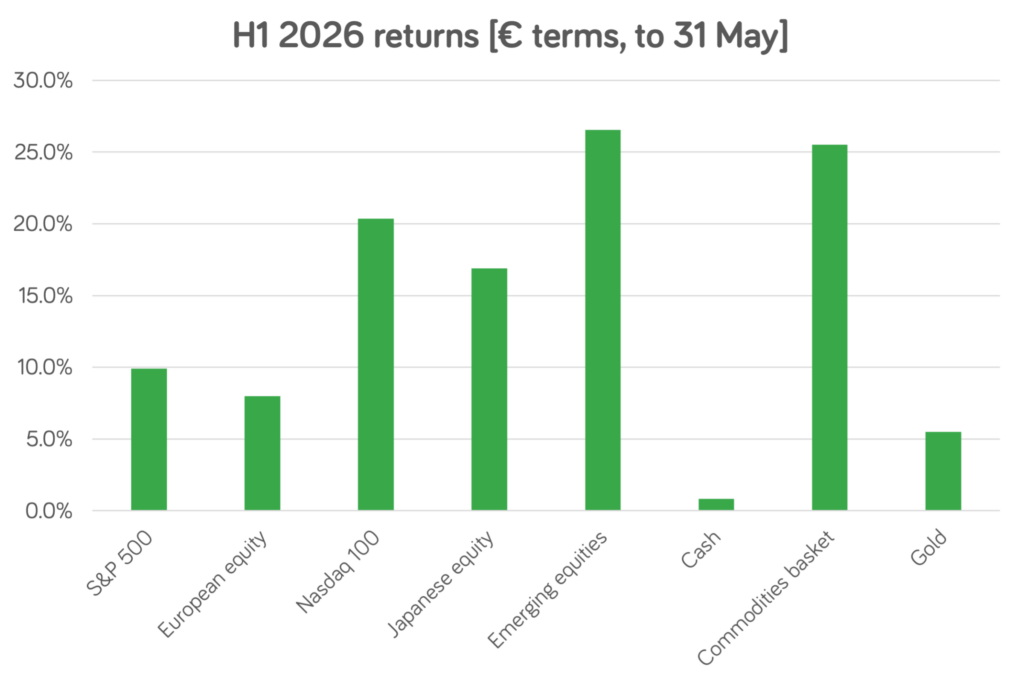

Regional winners in the first half of 2026

In stock markets, the big winner so far this year is clearly emerging markets. Driven by the infrastructure and component demands of the AI revolution, three emerging market companies have struck it big in 2026: Taiwan Semiconductor, Samsung, and SK Hynix. The latter two companies both more than doubled in market value in the first six months, as AI hyperscalers placed large orders for the chips and memory these Asian champions provide.

But other equity markets performed strongly too, as the chart shows, with all major markets displayed up at least 8% in the period to 31 May.

Of course these results hide a fairly serious hit in March in the wake of the Iran war, from which markets have largely recovered. For example, as war broke out, the S&P 500 index of top US shares posted its longest streak of losses since 2022.

However other asset classes offered a cushion to the drawdown seen in March – in particular oil and gas, which shot up as energy exports from the Middle East dried up. Energy (along with metals and foodstuffs) is a core component of the commodities fund we’ve highlighted in the chart. A commodities exposure delivered returns which were less correlated to equity markets and a key protection through the ups and downs of the first half of the year.

Where to from here?

The first half of 2026 is a reminder that markets rarely move in a straight line. Strong equity returns have come alongside war, energy shocks and renewed inflation concerns. As we look ahead to the second half of the year, investors face a market still offers opportunity, but with no letup in the volatility we’ve seen in the year to date.

One issue moving back to the top of the agenda is inflation. Many investors entered the year expecting central banks to continue cutting interest rates. Instead, higher energy prices and resilient economic activity have kept inflation stickier than expected, and central bankers appear in the mood to tackle it. The longer rates stay high, the greater the pressure on economic growth.

The AI boom continues to reshape markets. We are seeing increasing adoption as organisations figure out where AI can add value. Companies are deploying AI tools to improve productivity, automate processes and reduce costs. That trend is prompting enormous capital investment, which is turning into sales for suppliers of semiconductors, memory chips, data centres and energy producers.

There is another side to the AI story which could affect Ireland. As the technology becomes embedded in more businesses, we are seeing its impact on employment. While technology has historically created more jobs than it destroys, the transition can be painful. Ireland is not immune: there are growing fears that a significant number of jobs here are at risk as big tech cuts employment cost to invest in AI, with Meta the most prominent player implementing changes in the first half of the year.

Earnings, infrastructure and alternatives

For now, markets remain focused on the winners. The companies building the infrastructure behind AI, from chipmakers to power providers, continue to enjoy strong growth.

More generally, corporate earnings remain healthy. Despite geopolitical tensions, higher borrowing costs and ongoing uncertainty, many companies continue to deliver solid profit growth. Earnings are the ultimate driver of long-term market returns, and this resilience has helped support valuations.

Nevertheless, diversification remains as important as ever. One lesson from the first half of 2026 is that alternative assets can play a valuable role when traditional markets come under pressure. Commodities provided protection during the energy shock, while infrastructure assets benefited from rising demand linked to AI, electrification and energy security. Within equities, the S&P500 is not the only show in town – in fact other equity markets outperformed it in the first half of the year.

We continue to see advantage in maintaining exposure to alternatives such as commodities, infrastructure and selected metals. These assets can provide a hedge against inflation, offer returns that are less correlated with the stock market, and help smooth the journey when stocks become more volatile.

The second half of 2026 is likely to bring its own surprises. Inflation, interest rates, geopolitics and AI will all compete for our attention. But with corporate earnings holding up, the possibility of peace in the Middle East, further IPOs in the pipeline, and long-term growth themes in AI, emerging markets, still intact, opportunity remains. The key is not trying to predict every twist and turn, but building a diversified portfolio capable of weathering them.