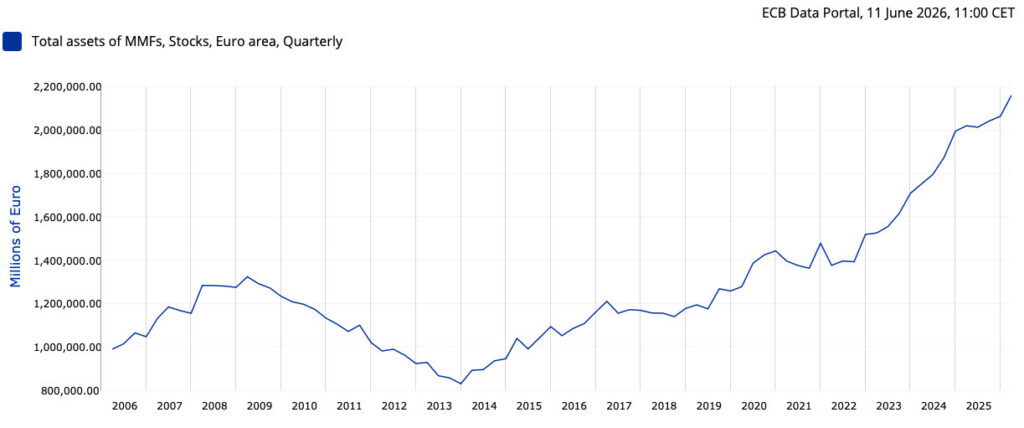

Investor interest in money market funds has become huge in recent years, with the value of the Euro money market reaching €2.1 trillion in March, up 42% in just three years. And with interest rates on the move again, the trend in the chart looks set to continue.

So what’s a money market fund, why would you want to invest in one? What are the advantages… and the risks? And how do you invest in a money market fund in Ireland?

Source: European Central Bank

Interest rates are rising… but not at a bank near you

In the wake of the Iran war, inflation is on the move again, and central banks are looking to raise interest rates to try to tame it. The European Central Bank’s deposit interest rate right now is 2.25%. – If you have a variable or tracker mortgage, you’ll soon notice the increased cost.

But while banks are often quick to raise lending rates, the interest you’ll receive on a cash deposit is still negligible. Despite a nudge from government a couple of years ago, the main banks in Ireland still offer no more than 0.25% for a €100,000 demand deposit, for example. (A couple of challengers like Moco are more generous).

But the collapse of SV Bank a couple of years ago reminded bank depositors that when you place money on deposit in the bank, you’re lending it to a business. And once the amount you have on deposit exceeds government-backed deposit guarantees, that loan involves some risk.

Beat the bank

The combination of poor deposit rates and reminders of the risks to cash deposits has prompted cash investors to look elsewhere. In particular, savers are moving money out of bank deposits, and into money market funds.

Right now, money market funds offer returns substantially in excess of what’s available on deposit at the Irish banks. One leading Eurozone money market fund from JP Morgan offers an annualised yield of 2.28% as at 11 June 2026, for example. And its US equivalent offers an even more enticing yield of 3.94% – although that involves currency risk to an Ireland-based investor.

It’s also possible to place your existing savings and pensions in a money market fund using Ireland’s major pension providers. For example, Zurich Life’s money market fund is currently yielding around 1.1%. This could be a sensible option, for example, if you’re approaching retirement.

What’s a money market fund?

A money market fund is an investment fund that invests mainly into highly liquid short-term loans. Typically the bonds a money market fund invests in are short-term loans to governments (also known as short bonds, gilts, or treasuries), banks (also known as deposits), and some large businesses (also known as commerical paper). Typically all the loans in a money market fund are repayable within a year, and often within days.

The aim of a money market fund is to offer a high degree of liquidity – that is, access to your money without delay – a low degree of risk to your capital, and an element of return.

Why would I want to invest in a money market fund?

People put their cash into money market funds for two very simple reasons.

Firstly, the prospect of a fairly secure, low-risk return. And secondly, because they know they can access their money quickly when they want it – whether that’s to turn it back into cash, or to invest into other opportunities when the timing seems right.

Sounds great – what’s the downside?

Of course, like any other investment, money market funds do come with some disadvantages. While they represent a relatively safe place for money in volatile times, the flipside is that over the long term, returns are low compared to other asset classes.

There’s also the fact that your money is not protected from capital loss in the way a bank deposit is (for the first €100,000 at least in the case of Irish banks). With money market funds, it is possible to make a loss.

Lastly, as with any investment, using a money market fund involves some cost, as a fund manager and an advisor will normally be needed to put the account in place.

How do I invest in a money market fund?

Having said all that, money market funds have their uses, and right now, the returns available significantly exceed what banks are offering. If you’re interested in putting some of your money to work, get in touch.