With the shops and restaurants shut, I’m saving much more money. So what should I do with my extra cash? Is now the time to invest?

– LB, Dublin

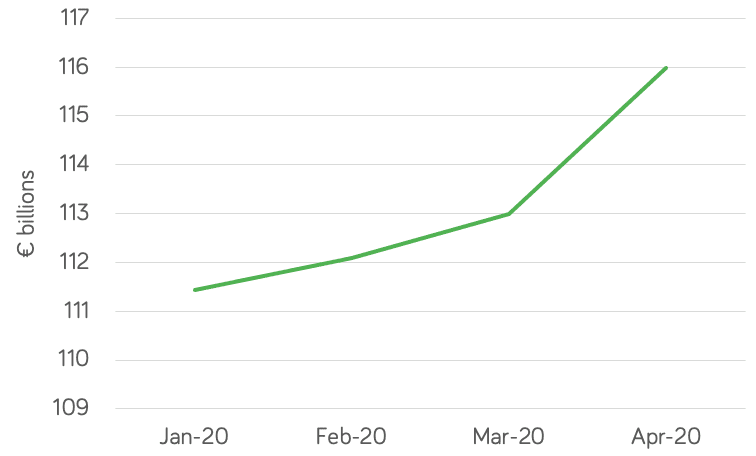

One of the side-effects of lockdown has been a huge increase in household savings. In fact, Irish households added €3 billion to their savings during April. That’s the biggest increase in a single month since the Central Bank of Ireland started to track data in this way back in 2003.

It leaves Irish bank savers with a record €116 billion of cash in the bank, as this chart shows.

It’s not hard to guess why: it’s harder to spend money when all the shops and restaurants are closed, and anyway, lots of people are rightly focusing on building up a cash buffer for the uncertain economic times ahead. The same instinct is prompting a lot of people to pay down expensive credit card debt and overdrafts, which is no bad thing.

But it’s also clear that another side-effect of everything we’ve been through is that bank interest rates are going to remain low for the foreseeable future. So that €3 billion is going to earn little or no interest for Irish savers.

Before you resign yourself to zero growth in your lockdown savings, here are five pointers to help you take charge of your savings plan.

1. It’s not an all-or-nothing decision

We’re the first to say that everyone should have a rainy day fund. Typically, it’s worth holding at least three months’ income in cash to cover unexpected costs. That gives you time and money, for example, to find a new job if you need to, or deal with an unplanned household cost.

But what if you’ve got a bigger rainy day pot? There’s no reason you can’t invest at least some of that into funds that can grow for you over time, and which you can access at short notice.

2. Keep the good habit of lockdown savings

Regular investing could be right for you if you want to keep up the good habits you’ve got into.

Lockdown is making us all re-assess our spending. For lots of people, there will be permanent savings, from less commuting, cancelled gym memberships, or even re-evaluating what spending is important and what is not.

If you want to keep those good financial habits and built up wealth over time, a drip-feed approach to investing could work.

3. Take out income protection or critical illness cover

The pandemic has made us all think about the value of our health. But illness can affect your finances at any time. If others depend on your income, it can have an even more serious impact.

That’s why having the right insurance cover is important to keep you going until you can start earning again or retire. Talk to Moneycube about your options today.

4. Spread your assets

Remember that the Central Bank of Ireland’s deposit scheme will cover savings up €100,000 with any single Irish institution. If you have more than that in a single bank or credit union, you might not be fully covered. So it’s best to spread your savings among various banks and credit unions. You can read about the deposit guarantee scheme here.

5. Invest a lump sum of your savings

There’s no doubt that markets have been volatile in the first half of 2020, and those ebbs and flows are likely to continue.

But as we’ve written elsewhere, there are several reasons why it remains worthwhile to invest your money in the current market, particularly if you do it in a risk-managed way, and are building wealth for at least 3-5 years.

If you’d like us to advise you, you can tell us your requirements online.