This guest blog comes from our friends at MyWallSt, the Dublin-based investing platform that has helped millions of people own their financial future with a suite of digital tools that make it easy to start investing.

In it, Michael O’Mahony explains two rules which have helped MyWallSt deliver market-beating returns year after year.

The stock market is now more accessible than it’s ever been. New technologies, the availability of information, fractional shares, and mobile investing have revolutionized the space, and now more people than ever before have been empowered to take control of their financial future.

However, with this new-found access comes a slew of pitfalls for inexperienced investors, not limited to speculation, day-trading, momentum investing, and the most recent head-scratching phenomenon of investing in bankrupt companies. I’m going to share with you the ethos that has guided MyWallSt to market-beating returns every year since we started.

Whether your mantra is to find, research, and invest in great companies or take a less hands-on approach and buy mutual or investment funds, the strategy remains the same. Those who invest with consistency and with a long-term outlook of 10+ years will vastly increase their likelihood of success in the market.

The historical returns of U.S. stocks

I recently came across an article from the Balance which analyzed the rolling returns of the S&P 500 over different time frames. From the piece: “Rolling returns do not go by the calendar year; instead, they look at every one-year, three-year, five-year, etc. time period beginning anew each month over the historical time frame selected.” Through this system, it was able to analyze the best and worst times to be invested in the stock market.

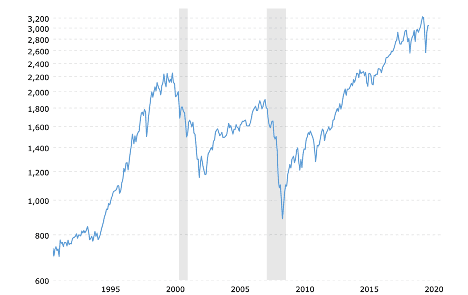

And believe me, there are bad times to be an investor. A quick glance at the chart of the S&P 500 for the last 30 years will give you a fair picture of how temperamental the stock market can be.

Historical Chart of the S&P 500. Image source: https://www.macrotrends.net/2324/sp-500-historical-chart-data

There are some fascinating insights in the article, and I would highly recommend reading it in its entirety, but what really stuck with me was the benefits of coupling consistent investing with a long-term outlook.

In the past 60 years of the S&P 500, the worst twenty-year time period was from June 1959 to May 1979. In this period, the index delivered an average return of 6.4% a year. So if you were unlucky enough to have invested $100 every month – a strategy called dollar-cost averaging which we highly recommend investors to practice – in the worst stock market in modern times, your consolation prize would be $46,162 — or a 92% return on your original investment. Not a bad lower limit to set, I think.

Investing the same way during the best twenty-year period, from April 1980 to March 2000 in which the S&P delivered an average annual return of 18%, would have bagged you a whopping $176,000, or 633% return on your original investment.

This investment strategy couldn’t be simpler and has shown historically that it works, yet why do we hear so many stories about retail investors losing money hand over fist?

The danger of short-term thinking

One of the biggest issues facing us retail investors is the very nature of stock market news. We are glued to the day-to-day ebb and flow of our portfolio and the market as a whole, flip-flopping from articles warning of a doomsday beckoning on Wall Street to those talking about the stock you simply must buy right now or you’ll be broke forever. Even quarterly earnings reports and the furor surrounding them should be little more than a mere talking point for long-term investors.

Ask yourselves the question: why do I invest?

I’m hoping it’s safe to assume that most of the answers will fall into the create long-term wealth/retire early/secure my financial future category. If this is the case, then let’s revert back to our twenty-year outlook. If an earnings report encapsulates the performance of a business for three months, this is just 1.25% of the time you plan on owning the stock. Why would such a minuscule portion of time have such an impact on your impression of the business?

The Art of Doing Nothing

The truth is that it’s incredibly difficult to be a long-term investor. It actually takes one of the most difficult and important skills of all to master: doing nothing. While it may feel like the most unnatural thing in the world to do, doing nothing is one of the key skills for ensuring long-term wealth.

If you ask any experienced investor about mistakes they’ve made in their investing career, our CEO and Chief Investor Emmet Savage included, all of them will be selling. Whether it’s trying to lock in some profits, putting too much importance on a few bad earnings reports, or losing faith in a good company, selling stocks is guaranteed to cost you more than buying them.

Of course, with investing nothing is black and white, and there will be times where you are forced to consider selling, but before you do, ask yourself the following questions:

- Has the business irreversibly changed for the worse from the one I first invested in?

- Is there a better place for my money right now than in this company?

If the answer to either of these questions is no, then it might be worth reconsidering that sell order. Remember, the only time you incur a loss is when you actually sell, up until then it’s just an underperforming stock.

Investing can be as easy or as difficult as you make it. If you spend hours every day on Bloomberg and Yahoo Finance, analyzing the most minor movements of your portfolio, you’re going to make it very difficult for yourself. If you invest in strong companies you believe in and maintain a long-term outlook, this investing lark becomes a lot easier.